George Anjaparidze, CEO and founder of Swiss economics and strategy think tank and advisory service Veritas Global, explains why a collaborative approach is urgently needed to ensure a sustainable future for aviation

We expect the impact of the coronavirus (COVID-19) will result in negative passenger air traffic growth in 2020 compared to 2019. This is despite a favorable global macroeconomic backdrop at the start of 2020. Our expectations are consistent with scenario 1 of the March 5 update by IATA on Financial Impacts of COVID-19, which estimates a loss in worldwide passenger revenue of 11%.

There are further risks to our outlook due to persistence of trade tensions and geopolitical risks as well as the possibility that COVID-19 epidemic worsens more than expected. Furthermore, in early 2020, some central banks chose to pursue less loose monetary policy, which could also be cause for concern. More broadly, we expect non-economic factors to increasingly influence performance of the aviation sector.

Coronavirus stings

2020 kicked off to a difficult start. According to the World Health Organization, as of March 4, COVID-19 claimed the lives of 3,198 people worldwide. The virus has also disrupted air transport networks and created an overall fear of traveling by air. As a result, this will be the first time the industry will post negative growth in passenger air traffic since the Global Financial Crisis.

Although we are in the early stages of outbreaks, we don’t expect the fear to persist in the medium to long term. Authorities are taking the necessary steps to contain outbreaks. Our most likely scenario assumes the epidemic of COVID-19 will be over in China by the end of April and by July in the rest of the world.

Nevertheless, the coronavirus will continue to be a major concern in the first half of 2020 but by the end of the year we don’t expect it to be on people’s minds.

Depressed growth

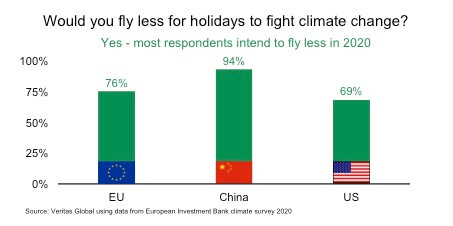

Unlike the coronavirus, climate change-related concerns will have a more lasting impact on air travel demand. A recent survey conducted by the European Investment Bank found that drastic and immediate shifts in consumer sentiment can be expected in 2020.

The survey found that 76% of Europeans, 94% of Chinese and 69% of Americans intend to fly less for holidays in 2020 as a way to help in the fight against climate change. These figures represent a significant boost to the ‘no fly’ movement.

The same survey identified that only about 36% of Europeans had reduced air travel in 2019 for climate change reasons.

Flight shaming movements are growing in momentum. Climate activists, like Greta Thunberg, are targeting flying with a ferocity not seen before. Many now consider aviation to be a dirty business. The green tide will continue to wash away demand unless industry becomes more proactive about strengthening its sustainability credentials.

The Carbon Offset and Reduction Scheme for International Aviation (CORSIA) offers some solutions. CORSIA is a global scheme that aims to address the growth from 2020 of airline CO2 emissions from international flights.

However, from the point of view of consumers there are two main concerns. One is that consumers are skeptical about the scheme – either because they don’t believe that it will be implemented, or they don’t understand (or agree with) carbon offsetting.

The second issue is that consumer concerns go well beyond the boundaries of airlines. Many consumers now expect to be informed of the sustainability credentials of the services they use throughout their journey. They want to experience sustainability as part of the travel experience.

To address the first concern of CORSIA skepticism, industry needs to make a concerted effort to fully implement CORSIA by launching ambitious within-sector emission reduction programmes as well as operationalising model offset projects.

In 2020, ICAO will be providing greater clarity on which offset mechanisms can be used for CORSIA compliance. Industry should take this opportunity and showcase projects that can be used to demonstrate the practicalities of sourcing offsets compliant with ICAO criteria and identified mechanisms.

In addition, there is a need for an education campaign that explains how offsetting works and why it is beneficial.

Addressing the second concern related to the desire of consumers to experience sustainability requires better climate disclosure practices and broader cooperation across the air transport supply chain. The physical journey starts and ends at an airport, where there are significant opportunities to do more to improve sustainability credentials.

One such opportunity is to do a better job at deploying renewable energy, in particular solar power. The airport industry should work together with key stakeholders, such as the International Solar Alliance, to identify the mix of policy incentives needed to better deploy solar power in a way that does not impose excessive financial burdens on airports while reducing their carbon footprint.

Ground handlers and other indirect service providers also need to provide greater visibility to consumers on their sustainability credentials.

Giving more information to consumers, combined with strengthening aviation’s sustainability credentials, should help improve consumer sentiment and restore confidence. It is time for the aviation industry to take a more proactive stance in 2020.